Brown No Longer: UPS Struggles for Relevance

Changing Logistics, Dispirited Leadership

Jim Casey, the UPS founder, once declared, "We do what we say." This promise, once the bedrock of UPS's success, now rings hollow as the company grapples with eroding market position, faltering financial performance, and a carousel of strategies that fail to deliver results.

The numbers from UPS's latest quarterly release paint a stark picture of a company in decline. In the second quarter of 2024, UPS reported consolidated revenues of $21.8 billion, a 1.1% decrease from the same period in 2023. More alarmingly, the company's consolidated operating profit plummeted by 30.1% to $1.9 billion, with adjusted consolidated operating margin at 9.5%. Diluted earnings per share fell to $1.65, with adjusted diluted earnings per share of $1.79 representing a staggering 29.5% drop from $2.54 in the previous year.

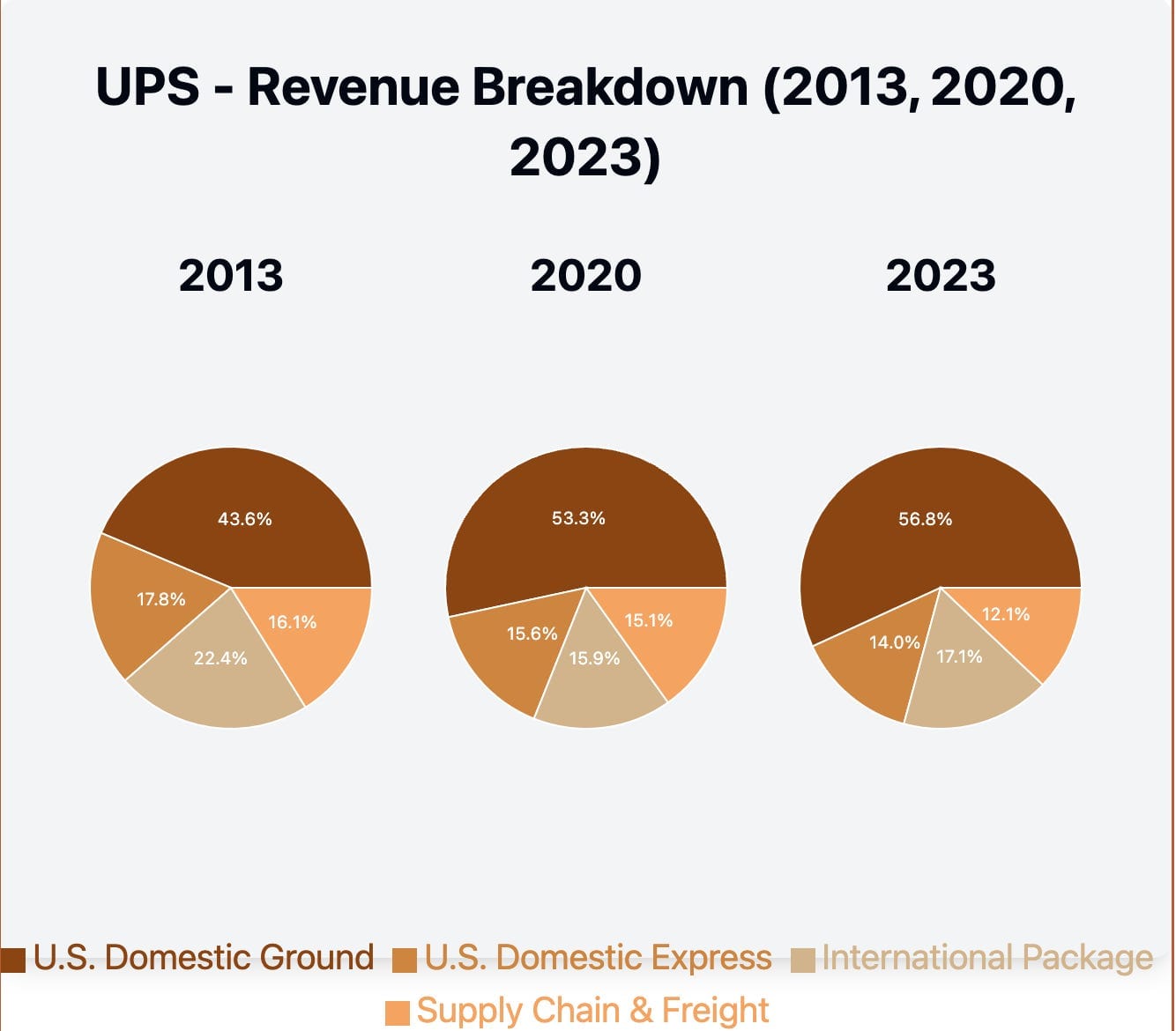

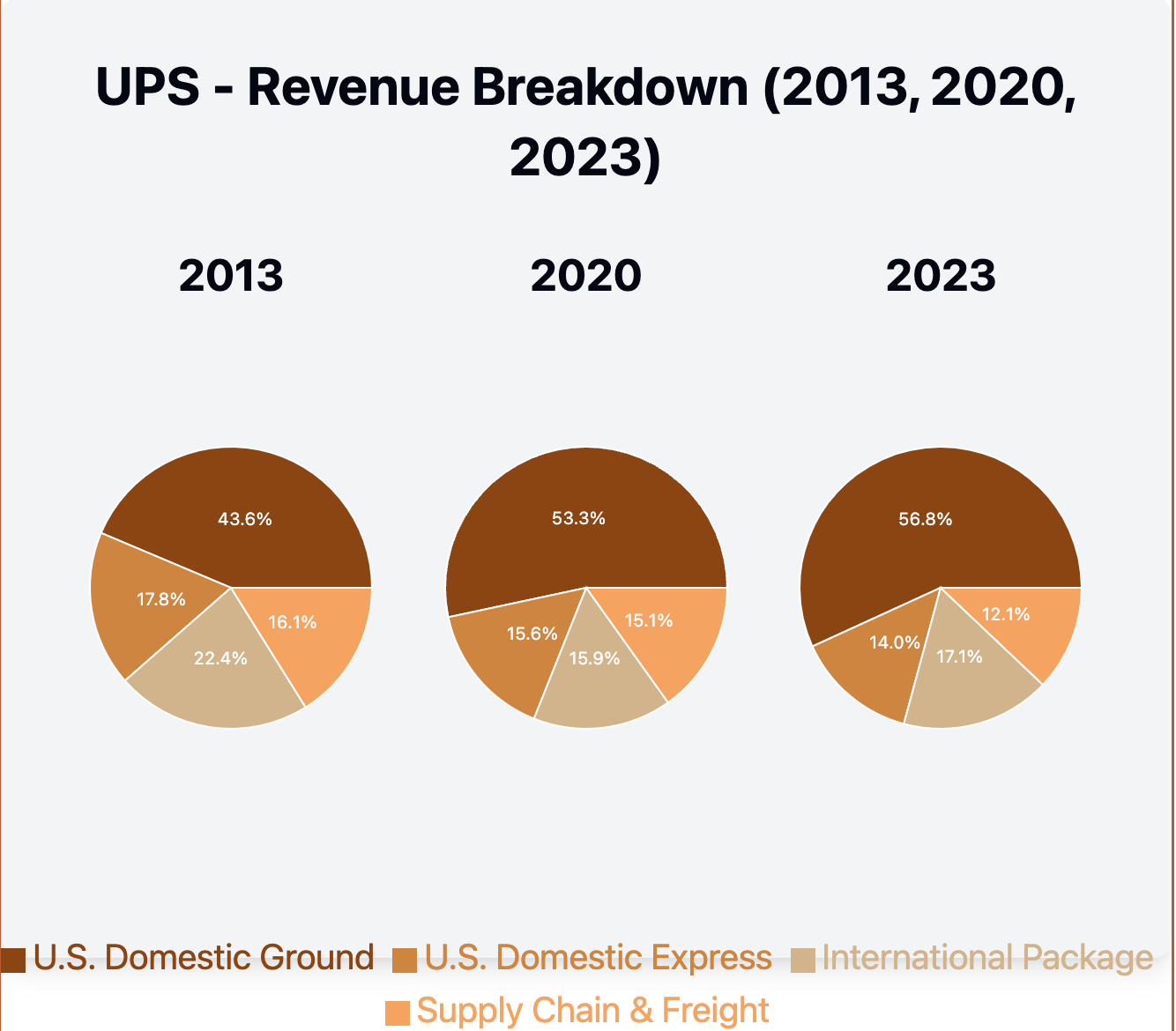

Since 2017, UPS has faced a stagnant package profile. While its duopoly with FedEx in the US allowed UPS to grow yields above inflation for most of the last decade, this advantage has evaporated in the face of economic uncertainty and multi-pronged competition. Amazon and USPS are targeting the low-end market, FedEx pursues high-value shipments, leaving UPS with no safe haven. The company's aspirations of becoming a diversified logistics powerhouse have faded, with over 70% of revenue now derived from domestic packages.

Three years into Carol Tomé's tenure as CEO, UPS finds itself neither bigger nor better. Despite Tomé's claim that the second quarter of 2024 marked "a significant turning point" with a return to volume growth in the U.S. for the first time in nine quarters, the financial results tell a different story. The U.S. Domestic segment saw a 1.9% decrease in revenue, driven by a 2.6% decrease in revenue per piece as it brought in more low weight B2C and saw a decline in higher yielding package volume. The International segment fared no better, with revenue decreasing by 1.0% due to a 2.9% decrease in average daily volume. The package growth on the backs of Shien and Temu appears to be hollow to many UPS watchers.

For this report, we conducted extensive interviews with current and former executives, industry analysts, and scrutinized decades of financial data. Our findings paint a clear picture:

- Since the collapse of the TNT acquisition in 2013, UPS has repeatedly failed to craft a coherent long-term strategy, instead repeatedly going to its domestic business and using price increases to improve profitability. This vacuum led to the unprecedented move of hiring external leadership starting at the end of the 2010's and into early 2020's, breaking from its tradition of promoting from within.

- These external hires, lacking a nuanced understanding of UPS's unique challenges and opportunities, repackaged old ideas (investing in healthcare, winning SMBs) rather than pursuing truly forward-thinking initiatives.

- Carol Tomé, famous at Home Depot as its CFO for declaring a "new strategy" to transform every 2-3 years, has taken the same approach at UPS. Hesitant to make bold moves, the company has settled for minor acquisitions like Happy Returns and MNX. While positive in their own right, these scratch-the-itch purchases are insufficient to stem the tide of market share loss.

The company's outlook for 2024 further underscores its struggles. UPS has updated its full-year consolidated revenue expectation to approximately $93.0 billion, with an adjusted operating margin of about 9.4%. These projections, coupled with the announcement of restarting its share repurchase program targeting $1 billion annually, are its latest attempts to appease investors and a sign of a management that’s out of ideas.

As we explore UPS's journey from a model of consistency to a company fighting for credibility, we'll examine its history, current challenges, and potential future paths. We'll analyze UPS's efforts to regain its reputation for reliability, a journey that will shape not just UPS's future but the entire logistics industry.

Carol Tomé states, "We're writing the next chapter in UPS's story, and it's going to be a great one." To many who follow and understand UPS deeply, this optimism is is exactly the kind of corporate spin they never thought they would hear from a UPS executive.

UPS: From Seattle Messenger Service to Global Logistics Powerhouse

The story of UPS is a quintessential American tale of innovation, perseverance, and adaptability. From its humble beginnings in 1907 as a small messenger company in Seattle, Washington, to its current status as a cornerstone of global commerce, UPS's journey mirrors the evolution of American business in the 20th and 21st centuries.

The Early Years: Laying the Foundation

In 1907, 19-year-old James E. Casey, along with his partner Claude C. Hopkins, founded the American Messenger Company with a $100 loan. Their venture, modest in scope, relied on bicycle messengers and a strong commitment to customer service, setting the stage for what would become a global logistics giant. By 1913, the company rebranded as Merchants Parcel Delivery, reflecting its expanding focus on package delivery. In 1919, the name United Parcel Service was adopted, marking the start of its national expansion.

Riding the Wave of Retail Revolution

From the 1920s through the 1960s, UPS capitalized on the rise of catalogue shopping. As department stores expanded their reach through mail-order catalogues, UPS became the go-to delivery partner. This prescient move laid the groundwork for the company's future success in the e-commerce era. During these decades, UPS expanded beyond Seattle, introducing new services and technologies. The 1930s saw the launch of UPS's first air express service, and by the 1940s, the company began its forays into international markets in Europe and Asia.

The post-World War II economic boom ushered in a new era for UPS. The 1950s saw the introduction of UPS's first trucking service, and by the 1960s, the launch of its air cargo service. These developments also marked UPS's shift towards business-to-business (B2B) shipping, a focus that would define its operations for years to come.

Navigating Challenges and Embracing Innovation

The 1970s and 1980s brought new challenges and opportunities. UPS faced increased competition from Federal Express and other express carriers, spurring the company to innovate. In 1982, UPS began overnight delivery of small packages by air, a service that became a cornerstone of its business model.

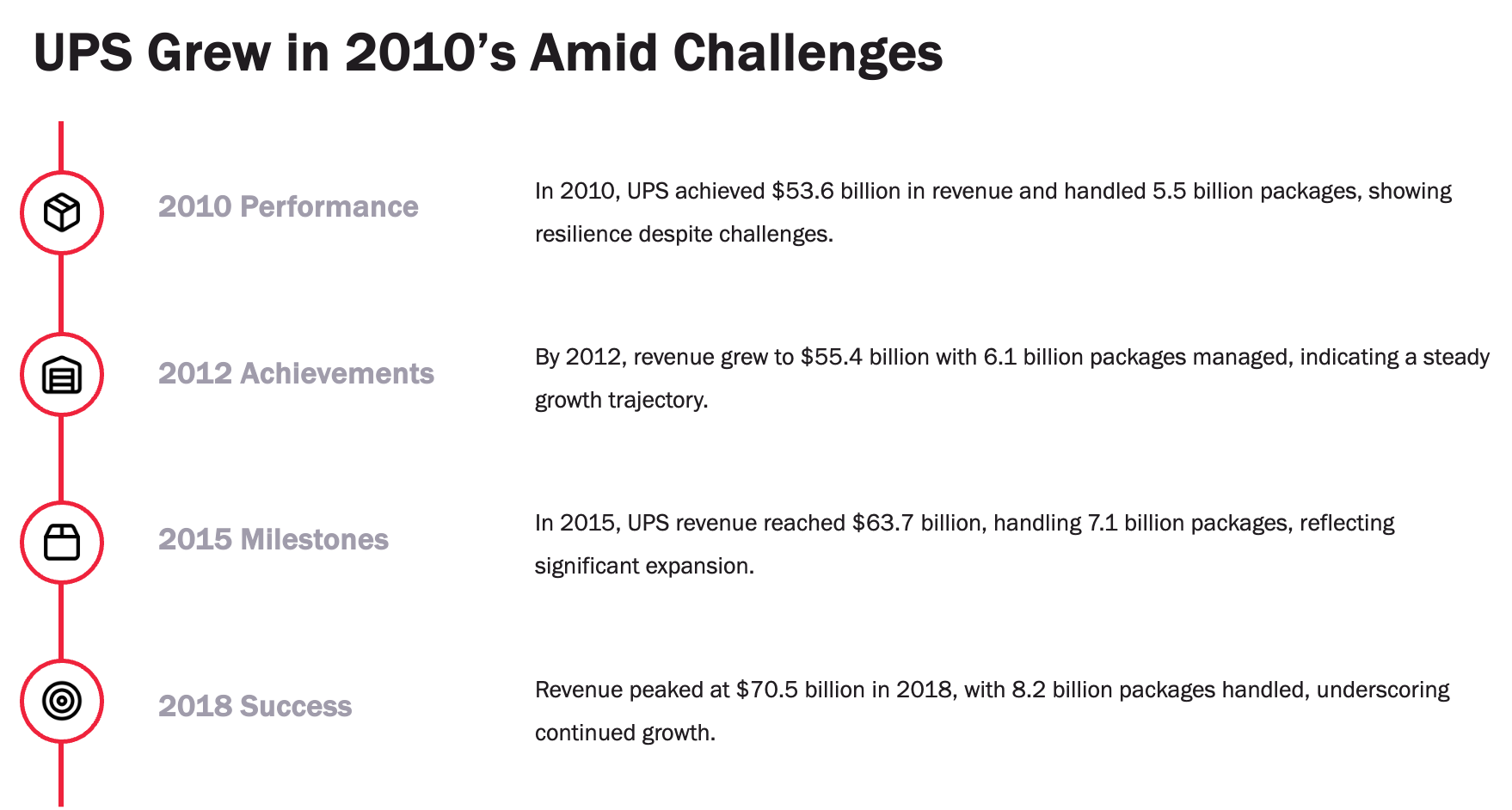

The 1980s also saw significant investments in technology, with UPS introducing electronic package tracking. This innovation was crucial in shaping UPS's future as a technology-driven logistics company. By 1984, UPS was reporting revenue of $7 billion, handling 1.9 billion packages on the ground and 55.6 million packages in the air.

The Global Era and the E-commerce Revolution

The 1990s and 2000s were transformative years for UPS, as it expanded globally and positioned itself for the e-commerce revolution. Online shopping surged in popularity, and UPS was well-positioned to capitalize on the increase in residential deliveries. However, this era also brought challenges. The shift from B2B to B2C deliveries put pressure on UPS's margins, as residential deliveries were typically less efficient and more costly than business deliveries. Moreover, the emergence of Amazon as both a major customer and a competitor forced UPS to rethink its strategy.

UPS also faced significant labor challenges during this period. In 1997, a 15-day nationwide strike led to agreements to create more full-time positions and increase wages, costing UPS an estimated $750 million. Despite these setbacks, the company continued to grow. By 2004, UPS's revenue reached $37.4 billion, handling 3.8 billion packages. Just two years later, in 2006, revenue jumped to $46.4 billion with 4.5 billion packages handled annually.

The Modern Era: Adapting to a Changing Landscape

In the 2010s, UPS's growth trajectory faced new hurdles. The company made a bid to acquire TNT Express in 2013, which would have expanded its European operations significantly. However, the deal was blocked by European regulators, leaving UPS to contend with a costly distraction. Meanwhile, rival FedEx successfully acquired TNT Express in 2016, only to find itself entangled in a challenging integration process. During this time, UPS managed to power through, focusing on its core operations while FedEx dealt with the complexities of merging with TNT.

However, by the mid-2010s, it became apparent that UPS was running out of fresh ideas. The company, long known for promoting from within, began aggressively hiring outside executives in search of new strategies. This marked a significant departure from its past, where homegrown leadership had been the norm. The new leadership, many of whom lacked a deep understanding of UPS's unique culture and challenges, struggled to bring about the transformative changes the company needed.

The COVID-19 pandemic in 2020 accelerated the shift towards e-commerce, giving UPS a short-term boost in volumes. By 2020, UPS reported revenue of $84.6 billion, handling 10.3 billion packages. In 2022, the figures grew to $100 billion in revenue and 11.5 billion packages handled.

The Ailments of a Logistics Giant

In early 2022, following the pandemic-induced high, UPS announced that it had accelerated its 2023 targets, bringing them forward by a year. Carol Tomé, the CEO, confidently declared the success of the "Better Not Bigger" strategy and introduced a new vision: "Bigger and Bolder." This new approach was supposed to be about taking bold bets and growing alongside customers who value UPS's complex network. However, just two years later, the company has lost 11% of its revenue and seen a 30% decline in profitability.

With revenue now dipping below $90 billion, Tomé launched yet another strategic plan in 2024, promising a 25% increase in revenue and a margin expansion from 8.9% to 13% by 2026. In simple terms, this is the same plan UPS had presented back in 2022 for revenue and profitability goals for 2024, now pushed back to 2024, now pushed to 2026. Sometimes, it’s clear you are dealing with a financial expert.

Despite these promises, UPS's stock has plummeted by 40% during this period, while its archrival FedEx has gained 25%. FedEx, although not immune to the downturn, had prepared better for the post-pandemic reality, grounding airplanes even as commercial capacity returned, and focusing on operational efficiency. The market's harsh treatment of UPS comes down to one key factor: a lack of credibility.

"UPS is essentially promising to square the circle," says a former executive who requested anonymity. "They’re targeting aggressive growth in healthcare, a notoriously complex sector, while simultaneously chasing high-volume, low-margin e-commerce business. It’s hard to see how these goals align. They are promising hockey stick growth without a clear strategy."

A hedge fund manager, who liquidated her entire UPS position after listening to the April presentation, was blunt in her assessment: “Carol’s pitch sounded like, ‘Trust me, bro.’ This is rich, considering the lack of delivery on previous promises.”

A high-ranking Home Depot executive who previously worked with Tomé noted, “Tomé loves grand strategies and can be very passionate about catchphrases, but she doesn’t always sweat the details. This approach works well during good times, but in tougher situations, detailed execution becomes paramount.”

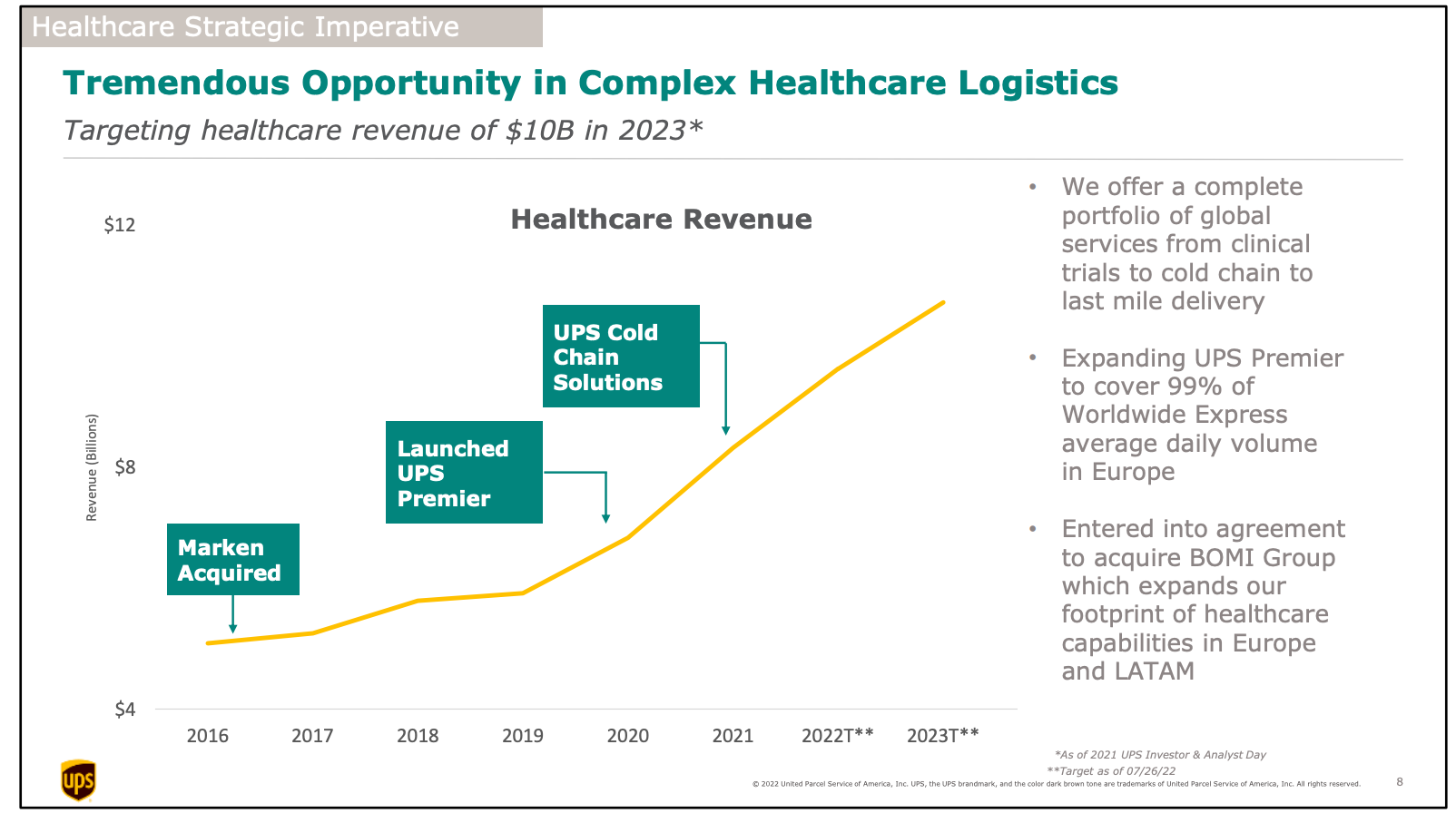

Unfortunately, reduced execution capability is a common criticism leveled at UPS's current management. UPS's new turnaround strategy hinges on two primary drivers: first, to continue leaning into price-insensitive customers by raising General Rate Increases (GRIs) annually, and second, to grow its healthcare segment exponentially, aiming to double revenue to $20 billion within the next three years.

The healthcare sector is indeed a lucrative market. Healthcare logistics, depending on how you define it is worth around $150 billion today and projected to grow into a $300 billion opportunity over the next decade. However, the sector is also fraught with challenges, including long-term customer loyalty and stringent regulatory requirements that make switching providers difficult. "When I was at UPS, we saw healthcare as a mosaic of opportunities," recalls a former healthcare division strategist. "Pharmaceuticals made up about 60% of our healthcare revenue. But it’s not just about moving boxes—it’s cold chain logistics, medical devices, and the highly profitable but small clinical trials segment. To double in size, UPS would need to excel in every single area and likely acquire other companies to achieve such rapid growth."

The skepticism surrounding UPS's ability to achieve these targets is understandable. "It’s possible to achieve such growth in this market, but not without significant capital investment, which UPS seems hesitant to commit to," continued the former strategist. "The notion of doubling revenue without substantial capital outlay while simultaneously improving profitability, that too in just 3 years? Doubt it.”

The market doesn’t completely write off UPS when it comes to healthcare, either. Indeed, it has outcompeted many, including both FedEx and DHL in this space. But this executive provided additional context: “The earlier growth from $5 billion to $10 billion was impressive. I was there for it. They fail to tell the market that while we doubled the healthcare business, part of it was the market and part of it was smart acquisitions. There were some very clear strategies, which I just haven’t heard so far from the UPS management."

Challenges also loom large in the e-commerce sector, where UPS has been courting high-volume but low-margin clients like Shein and Temu. This strategy has led to an increase in volume but at the cost of profitability. "It’s a Faustian bargain," says an e-commerce logistics consultant with a large following on LinkedIn. "About 20% of UPS's e-commerce revenue—yet 50% of the volume—comes from large marketplaces like Amazon, Shein, and Temu. These players demand rock-bottom pricing, squeezing UPS’s margins. Meanwhile, small and medium-sized businesses, traditionally a profit engine for UPS, are increasingly being courted by competitors. GLS is expanding. Even Ontrac has almost a full National coverage. Not saying there’s a huge competition today, but it’s not just FedEx that’s putting the pricing pressure on UPS for these SMB customers."

The reliance on low-margin e-commerce deliveries is becoming a significant concern, as reflected in UPS's income statements where volume is up but yields are down—exactly the opposite trend seen at FedEx. "We’re building a growth strategy on quicksand," warns a former UPS policy advisor. "A shift in U.S. leadership and subsequent changes to Section 321 legislation could cause this volume to evaporate overnight."

Meanwhile, UPS's leadership under Carol Tomé continues to face mounting criticism. Tomé’s "Bigger and Bolder" mantra, barely two years old, has been quietly replaced by a growth-at-all-costs approach. "It’s starting to feel like we’re playing strategy bingo," quips a former UPS manager. "What’s next? ‘Bigger and Better’? In logistics, you can’t change course on a whim. Our entire operation was geared towards ‘Better Not Bigger.’ Now we’re supposed to pivot to aggressive growth? It’s not that simple."

These strategic shifts are occurring against a backdrop of stagnating volume and growing discontent among UPS’s workforce. Labor unrest has intensified, particularly among part-time employees who feel underpaid and undervalued. "Part-time employees work extremely hard to make this company profitable, and we deserve to share in that success," stated a UPS employee and member of Teamsters Local 396.

The labor tensions reached a boiling point during the 2023 contract negotiations when UPS walked away from the bargaining table, refusing to present a final offer to the Teamsters union. This move sparked widespread protests and practice pickets across the country, further straining the company’s already tense labor relations. Although UPS eventually secured an agreement with the Teamsters in 2023, it came at the cost of losing profitable business that has yet to return.

Yet, in the company’s last earnings call, Brian Newman, the outgoing CFO, remained optimistic. "We’re not just adapting to the market," Newman stated. "We’re working to shape it. Our focus is on creating value, not just moving packages." However, a senior financial analyst expressed disappointment, saying, “We bought into the razzle-dazzle and gave UPS too much credit in 2022. The signs were there in their February investor update where Tomé took credit for everything except causing the pandemic.”

Future and Recipe for Success

Indeed, UPS has lost much ground and time during the past 2 years, as Amazon FedEx and others have aggressively taken capacity out and adjusted their networks for future. A former executive, now retired, remarked: "We brought back executives from retirement to lead the company, instead of picking an insider as we have done before. There are some brilliant strategists out there, but bringing in Carol Tomé, who had no prior CEO experience, was a gamble. Boeing did something similar… we’ll see how it works out for them, but at least they have brought in an operator. UPS is fundamentally an operations company. Look at what happened when Paul Oberkotter was replaced by his brother Harold. Paul had the charisma, but it was Harold, with his decades of operational expertise, who stabilized the company and built a foundation that still supports UPS today."

Central to UPS's future success is navigating the delicate balance between cost control and investment in new growth areas. While the company's broader strategy to grow its healthcare logistics is sound, achieving its ambitious target of doubling healthcare revenue to $20 billion by 2026 will require more than just expansion—it will demand a willingness to take risks and make bold strategic investments. A shipping expert we spoke with noted, "Healthcare logistics is not just about moving packages; it's about mastering the complexities of cold chain and time-sensitive deliveries. Above all, you have to master compliance and regulations. UPS needs to get uncomfortable, and that means making significant investments where others might hesitate."

Another area, we believe UPS has been timid is international. Despite its focus on healthcare, UPS's retreat from international markets is concerning. The company’s reluctance to compete aggressively on the global stage, especially in Europe and Asia, is puzzling. "If Harris wins the election and pushes for normalization with China, UPS could find itself scrambling to regain ground it has ceded," a market analyst warned. The underinvestment in Europe also limits UPS’s potential for diversification and growth in healthcare logistics—a sector it desperately needs to dominate.

In the domestic market, UPS faces the dual challenge of maintaining profitability in the e-commerce sector while competing against giants like Amazon, which are increasingly managing their own deliveries. The company's e-commerce operations, now a significant portion of its overall volume, must evolve. "UPS needs to leverage its vast network and technological capabilities to offer services that stand out in a crowded market. Happy Returns is a good start, but it won't be enough to anchor long-term growth," another industry insider suggested.

For a company as large and as storied as UPS there are opportunities, but it has to start at the top. "UPS needs someone who understands the operations at a fundamental level and isn’t afraid to push the company into uncomfortable but necessary territory," the former executive added.

We agree: it’s time for Carol Tomé to go.