AMD: A Challenging Downcycle Emerging

AI investments to top before AMD can make hay

In our recent report, we examined NVIDIA and the significant pressures impacting its fundamentals. Since the release of our Report, our analysis has been picked up by other commentators who are now echoing what we concluded: the peak of AI-driven GPU demand may be near, and we will see a declining demand in 2025. This viewpoint is supported by observations from major industry players such as Alphabet and frank remarks from META's CEO, Mark Zuckerberg. Analysts and experts we spoke with suggest that industry is transitioning from a phase of intense capacity building for training large AI models to a focus on inference, leading to a reduction in orders. This shift will likely reverse the double orders from the hyperscalers, and a decline in revenue for AI leaders such as a NVIDIA and AMD.

Building on this groundwork, we now extend our focus to Advanced Micro Devices (AMD), a key player in the semiconductor industry that’s the center of the current boom. Despite shaving one-third its value since March, our research indicates that AMD stock will decline potentially another 50% from here. “There is a remote possibility for strong growth in 2024, but it is contingent upon an unlikely expansion in the demand for generative AI training—a scenario that we do not foresee. By 4Q, we expect to shift our focus to inference, shifting the same capacity we have built, and start to shift some of our 2025 orders back to 2026 and beyond,” told us a buyer at top-5 buyer for the AI chips. This Report draws from over 30 interviews with a broad spectrum of individuals connected to AMD, including current and former employees, analysts, and investors. If the analysis holds, we anticipate AMD losing $100-$150 billion in its paper value over the course of next 12 months.

Strategic Insights Report is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

Strategic Insights Report is powered by our readers. We provide exclusive and comprehensive coverage of crucial yet often overlooked business and political developments, including our detailed economic analyses based on hundreds of expert interviews. Subscribe today to join a community of forward-thinking professionals who depend on our indispensable business insights.

Insiders predict a fierce price war in the GPU/AI chip market by 2025, a development that would likely hit AMD harder than its competitors, including NVIDIA. This analysis aims to provide a comprehensive look at AMD's strategic positioning and the potential challenges it faces in a rapidly evolving industry landscape.

AMD's Strategic Challenges Amidst GPU Market Dynamics

Advanced Micro Devices (AMD) is currently navigating challenging waters in the GPU market, holding the second-largest market share in an industry facing imminent contraction. This scenario mirrors historical challenges, reminiscent of 1999 when AMD faced stiff competition from Intel's Celeron in the lower-end segment, turning a potentially strong decade into a prolonged struggle. An experienced investor in the semiconductor space reflected, "Just like in 1999, the industry does not signal declines; they appear abruptly, turning what is specialized today into tomorrow's commodity. This is not the first time the semiconductor sector has overextended itself."

Presently, projections point to a significant reduction in GPU demand by 2025. This downturn follows a period of intense investment by tech giants such as Meta, Alphabet, Amazon, and Microsoft in AI training infrastructure, investments that are now shifting towards inference phases, reducing the need for further expansive hardware outlays. "The market's past explosive growth in GPU demand is unsustainable. With the current infrastructure, the need for AI training chips is expected to drop by as much as 15-20% by 2025, a decline that could deepen with worsening macroeconomic conditions," explained an industry analyst from a leading tech analysis firm.

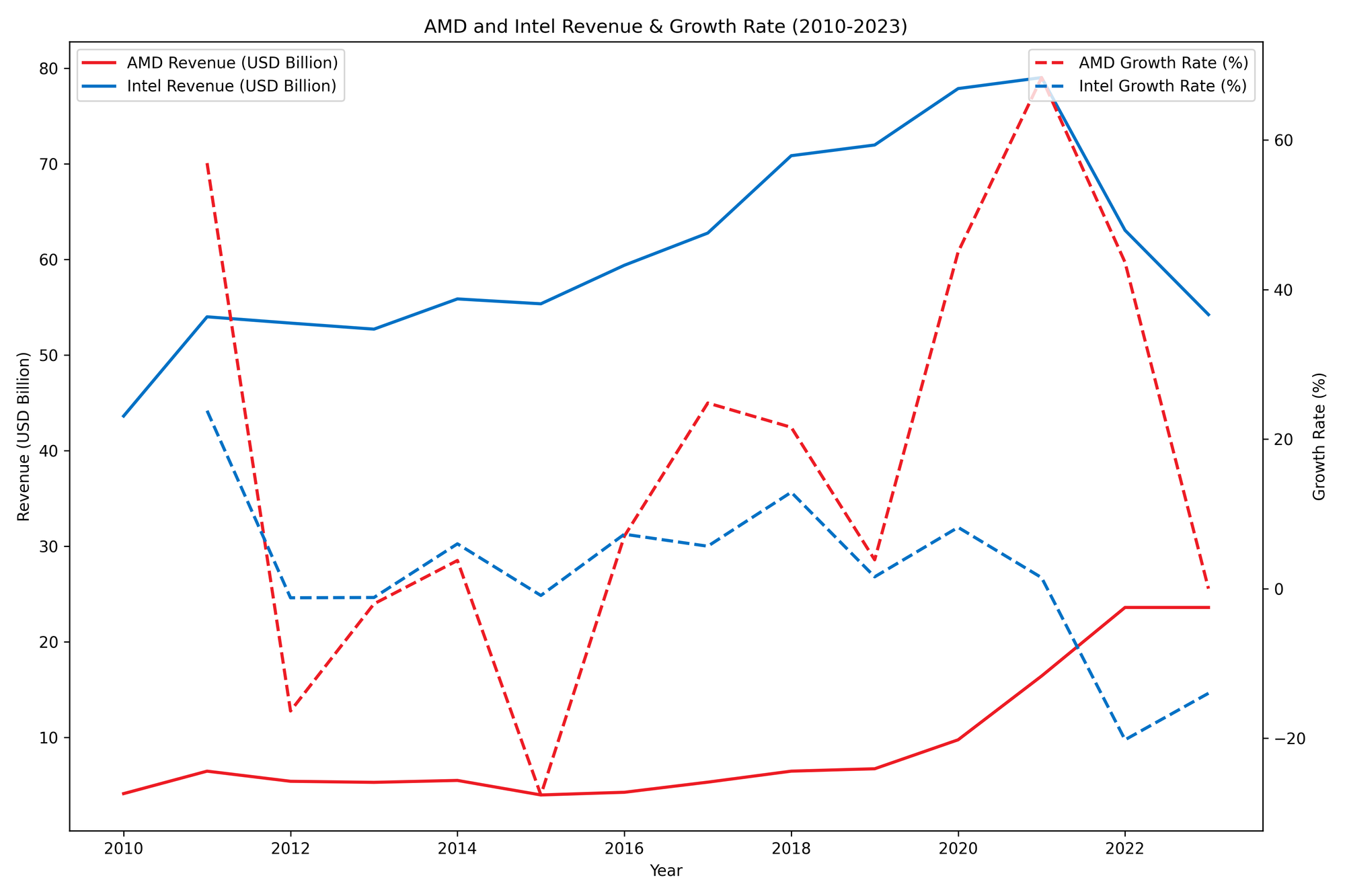

This anticipated decrease arrives at a critical juncture for AMD, which has been ambitiously expanding its presence in the high-margin AI chip sector to challenge NVIDIA's dominance. Recent financial reports from AMD reveal troubling signs: a 4% decrease in year-over-year revenue to $5.8 billion and a substantial 24% reduction in net income to $667 million for the last quarter of 2023. These figures are concerning, especially given AMD's strategic emphasis on AI and data center markets, areas that have yet to deliver the projected financial benefits.

A senior portfolio manager at a prominent investment firm highlighted the disparity between AMD's growth narrative and its financial outcomes, noting, "AMD has constructed a compelling narrative of growth and expansion, yet the financials tell a different story. The company's operating margin has shrunk from 22% to 16% within just a year, indicating the unsustainability of its aggressive expansion strategy in the AI sector."

Moreover, AMD's increased R&D spending, which surged by 35% to $1.4 billion during the same period, is crucial for its AI ambitions but is also exerting significant pressure on its profitability. A seasoned semiconductor analyst from a major financial institution, who has tracked AMD for over a decade, pointed out, "AMD is in a precarious position. Their hefty investments in AI technology to compete with NVIDIA are heavily taxing their financial health. It's uncertain whether these investments will convert into market-leading products and significant revenue growth before the market contracts."

But before we talk about the troubles, we have to talk about how we got here.

AMD: Lisa Su’s Leadership Lessons

Lisa Su is not what you might expect from a high-powered tech CEO. She doesn't resort to throwing chairs or raising her voice to command attention. Instead, her leadership style is marked by a steady, consistent presence and a relentless drive for innovation. Under her guidance, AMD has experienced a radical transformation. Before Su's tenure began in October 2014, AMD often found itself as the perpetual runner-up to Intel. Since then, the company has not only surpassed Intel in market valuation—now sitting at twice Intel's worth—but also quintupled its revenue, all while Intel faced declines during the same period.

The narrative of Advanced Micro Devices (AMD) under Dr. Lisa Su's leadership showcases a remarkable turnaround and strategic reorientation. When Su took the helm, AMD was wrestling with significant financial difficulties and shrinking market share, particularly in the fiercely competitive arenas dominated by giants like Intel in CPUs and NVIDIA in GPUs. Su's ascendancy marked a pivotal shift, repositioning AMD from the brink of obscurity to a path of robust recovery and impressive growth.

Dr. Mark Thompson, a technology historian at MIT, remarked on the state of AMD prior to Su's leadership: "When Lisa Su took the helm, AMD was in dire financial straits. The company was bleeding cash, and its market share was shrinking. It was a critical moment, with many speculating about the company's potential bankruptcy."

Under Su's leadership, AMD focused on high-performance computing, streamlined its operations, and cultivated a culture of innovation. One of Su's first significant decisions was to exit the dense server business, a move that, while controversial, allowed AMD to reallocate resources towards more promising areas. A senior analyst at a prominent tech lab noted, "Exiting the dense server business was a decisive and strategic move by Su. It highlighted her willingness to make tough, forward-looking decisions that were necessary to stabilize and reposition AMD for future growth."

The fruits of this strategic realignment began to materialize with the launch of AMD's Ryzen CPUs and EPYC processors, marking a return to competitiveness in the processor market. These products, based on the revolutionary Zen architecture, signified AMD's renewed ability to challenge Intel's dominance. A former AMD engineer intimately involved with the Zen project shared, "The development of the Zen architecture was a turning point for AMD. It was a make-or-break project, and Lisa Su's leadership during this period was instrumental. She provided the resources and support needed to innovate, despite external pressures."

Financially, AMD saw a dramatic turnaround under Su's leadership. From a struggling entity with a stock price lingering around $2 per share in 2014, AMD's market capitalization soared, reflecting renewed investor confidence. By 2019, AMD had not only returned to profitability but also seen its stock price increase exponentially.

In 2020, AMD made another bold move under Su's guidance with the acquisition of Xilinx for $35 billion, the largest in the semiconductor industry at that time. This acquisition was aimed at broadening AMD's technological horizons, particularly in adaptive computing, which is crucial for future tech trends such as 5G, automotive, and edge computing. A Professor of Business Strategy at Stanford University analyzed this acquisition, stating, "The Xilinx acquisition is a testament to AMD's strategic vision under Lisa Su. It significantly diversifies AMD's portfolio and enhances its capabilities in emerging technological areas."

Throughout these transformations, Su maintained a focus on technological innovation and market expansion, which was crucial as AMD navigated its recovery and growth phases. The release of new CPU and GPU architectures under her leadership has enabled AMD to capture significant market share from its competitors and positioned the company as a leader in the semiconductor industry.

As the calendar turned from 2010’s to 2020’s, it was clear Su had defeated its once nemesis, Intel, and was raring or to fight another innovator NVIDIA.

Analyzing AMD's Current Challenges and Future Opportunities

AMD has adopted a strategy with its GPUs and AI chips that echoes its approach in the CPU market: cheaper, if not always better. This tactic has positioned AMD as a strong contender in the GPU space, second only to NVIDIA. “AMD is always in conversation, especially when price is a concern,” commented a procurement leader at a hyperscaler.

However, being in the conversation is not the same as winning the business. While NVIDIA has impressively been doubling its revenue annually in recent times, AMD's revenue growth has plateaued as the company focuses on developing increasingly sophisticated chips to challenge NVIDIA's dominance. Under the leadership of Lisa Su, AMD confronts a multifaceted set of challenges and opportunities within the semiconductor industry, particularly in the AI chip sector. “We are becoming a software company, and the talent doesn’t come cheap,” lamented a senior AMD executive. “We are catching up to NVIDIA, but not fast enough.”

According to experts we've consulted, AMD may struggle to capitalize on the current market boom as effectively as NVIDIA, especially as the market is expected to shift from being supply-constrained to potentially oversupplied by 2025. This anticipated change, coupled with escalating demands for AI capabilities and an uncertain global economic climate, presents a mix of potential risks and strategic opportunities. AMD must navigate these dynamics adeptly to sustain its growth and solidify its market position.

“The GPU market is on the brink of a significant contraction by 2025, anticipated due to a stabilization in the demand for AI training that previously fueled rapid market expansion.” A senior executive from a major cloud service provider elaborated, “We are reconsidering our hardware needs based on current AI infrastructure. There's a growing sentiment that the intense investment phase in AI training might give way to a period of optimization and efficiency, potentially leading to reduced hardware demand.”

This forecasted downturn poses a challenge for Advanced Micro Devices (AMD), potentially dampening its recent successes in the GPU sector. Despite launching promising products like the MI300X AI accelerator chip, AMD is confronted with the dual challenge of capturing market share from NVIDIA and adjusting to a softer market demand. A Director of AI Research at Stanford commented on the situation, "AMD's MI300X is a technologically impressive product, but overcoming NVIDIA’s entrenched market presence involves more than just superior hardware. It requires building a robust ecosystem around these products, which is a significant challenge."

Moreover, AMD’s financial health is a critical area of focus as it heavily invests in R&D to innovate and stay competitive. Although the company has seen impressive revenue growth and a significant increase in market capitalization, reflecting strong investor confidence, these accomplishments come with heightened expectations for performance and profitability, especially in the highly competitive AI chip market. A financial analyst from a top investment bank provided insights, stating, "AMD has shown remarkable resilience and strategic savvy in its financial operations. However, as the market conditions evolve, especially with potential downturns and price wars in the GPU market, AMD needs to maintain a delicate balance between investing in innovation and managing its financial resources prudently."

Navigating the Shifting Landscape of AI and GPU Markets

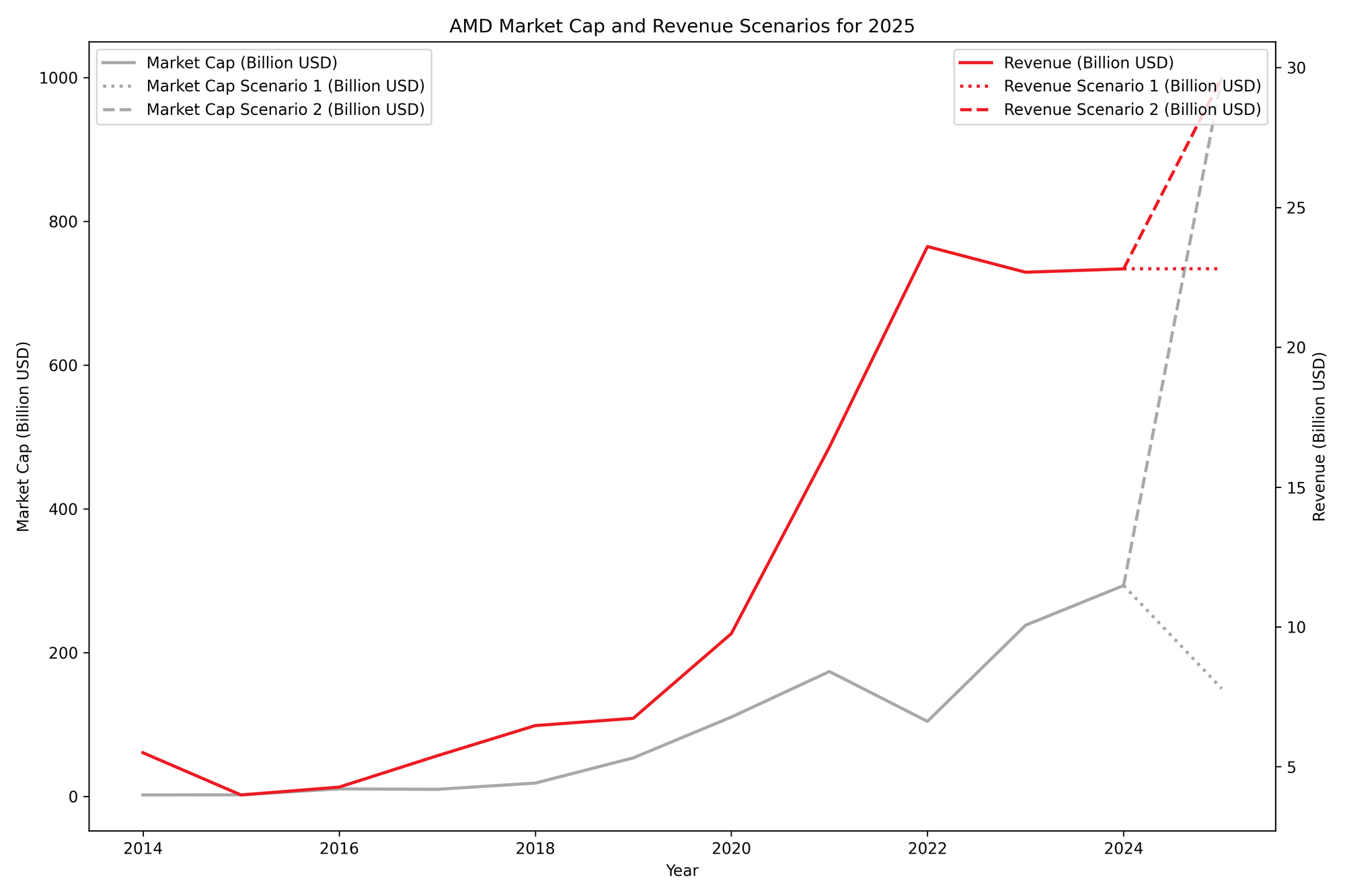

Let’s be clear as we conclude this Report: Lisa Su is a generational CEO. She transformed AMD from an also-ran to a leader in semis. There is an awful lot of respect for what she has achieved, and at 54, she will likely cotninue to have a tremendous impact on this industry in the years to come. That aside, it's evident that the company is positioned at a facing intense years which will define how we remember Su’s legacy. While AMD has achieved significant strides under Lisa Su's leadership, transforming from a peripheral player into a serious competitor in the semiconductor industry, how it manages the downturn in demand of AI chips will determine if AMD becomes a trillion dollar company in next 5-7 years as some predict or a sub-100 billion, as others contend.

The AI chip market, which has been a significant growth driver for AMD, is showing signs of stabilization. This stabilization is not merely a pause but a shift towards optimizing existing capacities rather than expanding them. Major industry players are now focusing on making AI operations more efficient, which could reduce the need for frequent hardware upgrades and, consequently, dampen the immediate demand for new GPUs. “Procurement at this sale can be very opaque to outsiders, but the cycles will become very apparent in near future,” predicted a Consultant who helps optimize data center capacity. “It’s not terrible if you overshoot. Look at Amazon, they did overbuild during Covid, and it took 2 years to digest all that overcapacity, but they have been growing again. There will be an oversupply soon, followed by price wars, followed by losses for AMD. Long term, they will win if if they continue to innovate and knowing Su, we know she won’t stop innovation.”

Financial analysts and industry experts are raising concerns about AMD's valuation, however, which currently reflects optimistic growth expectations that may not align with the evolving market realities. The potential for a market contraction in GPU sales due to these optimizations poses a direct challenge to AMD’s revenue streams in the coming years. An industry analyst from a leading financial firm noted, "While AMD has been a growth favorite, the market dynamics suggest a cooling period where profitability and revenue growth could face downward pressures. Yes, it’s down 30% from the top, but we are nowhere close to done, yet. I will be buyer at 60 bucks." The stock is trading at $140 at the time we published this Report. While nobody knows if the stock will fall as low as $60, analysts we spoke with generally suggested caution.

“If the market holds up, we may see AMD valuation explode the next year. But far more likely is a drop,” noted a financial analyst who provided two possible scenarios: a 20-30% revenue growth in 2025 vs a 20% decline, putting the odds of latter at 4 to 1. “With those odds, I am not recommending my clients to invest in AMD right now.”

“When NVIDIA sneezes, the market catches a cold, and AMD catches a pneumonia. Expect a giant strain for AMD,” suggested another CIO at a Tech focused hedge fund, who has added to Intel, but otherwise trimming their investments in semis space.

In response to these immediate market challenges, AMD may need to recalibrate its strategy. The focus may shift from aggressive market capture to enhancing operational efficiencies and protecting profit margins amid potential price wars. This could involve strategic adjustments in production to manage oversupply risks and renewed efforts in R&D to innovate within the current product lines to add value beyond mere hardware performance. While the market would love these actions, we see a concern with long-term position if Su and her leadership team trim these long-term investments in face of a declining demand.

Furthermore, AMD must strengthen its relationships with key players in the industry and begin to translate strategic discussions into tangible revenue streams. Securing even a small percentage of the AI market share in the upcoming quarters could provide a solid foundation from which AMD can effectively compete. A technology strategist emphasized the strategic approach required, noting, "AMD’s path forward will require a nuanced balance of innovation, market adaptation, and strategic partnerships. Initially, they might need to 'buy' their way into the market, as they did successfully in the data center sector in the early 2010s, which yielded positive market responses later in the decade. Investors need to understand that investing in semiconductors is not for the faint-hearted; these investments can take many years to materialize."

Looking ahead, the semiconductor industry, particularly the sectors focused on AI and high-performance computing, will continue to evolve rapidly. The oversupply scenario is not a foregone conclusion. A new breakthrough or other market dynamics such as projected rate cuts may trigger the next wave of investments, but the investors and experts we spoke with suggest that the next set of innovations will shift from hardware to software, and as it has happened in the prior cycles, we will suddenly find ourselves in an oversupplied market. Such prospects are not great for AMD investors, unless they are investing for the next 5-10 years and not 12-24 months.

An analyst who covers the company and has been warning us about the coming downturn had the last word: “AMD is a tremendous competitor, but if the market evolves as we think it will, you will have better opportunities to invest in it the next 12 months.”

Strategic Insights Report is a reader-supported publication. To receive new posts and support our work, consider becoming a free or paid subscriber.